Python | 风控决策引擎实战:从规则链到多源评分融合

- 2026-06-28 01:49:29

QIAN

数据

6

月

7

日

2026年

先验直觉:决策引擎不是"一套规则",而是一个贝叶斯决策机器——它把每一笔申请变成后验概率,然后根据损失函数做出最优分类决策。规则链只是它第一层的传感器,评分模型是第二层的透镜,决策矩阵是最后的扳机。

一、引言

1.1 从规则到决策

在信贷风控中,一笔申请从进入系统到输出"通过/拒绝"的决策,通常经过三个阶段:

申请进入 │ ▼┌──────────────┐│ 规则链 │ ← 硬性拒绝:黑名单、年龄<18、多头超限│ (硬性规则) │ 输出:拒绝(不进入后续流程)└──────┬───────┘ │ 通过 ▼┌──────────────┐│ 评分模型 │ ← 评分卡 + XGBoost/LightGBM│ (软性分数) │ 输出:信用评分└──────┬───────┘ │ ▼┌──────────────┐│ 决策矩阵 │ ← 多源分数融合 + Cutoff阈值│ (最终决策) │ 输出:通过 / 人工审核 / 拒绝 + 额度└──────────────┘这个三层结构就是风控决策引擎的骨架。它不是一个模型、不是一个规则集,而是一个完整的决策系统——在每一层都有一套数学规则决定"接下来怎么办"。

1.2 为什么需要系统性的决策引擎?

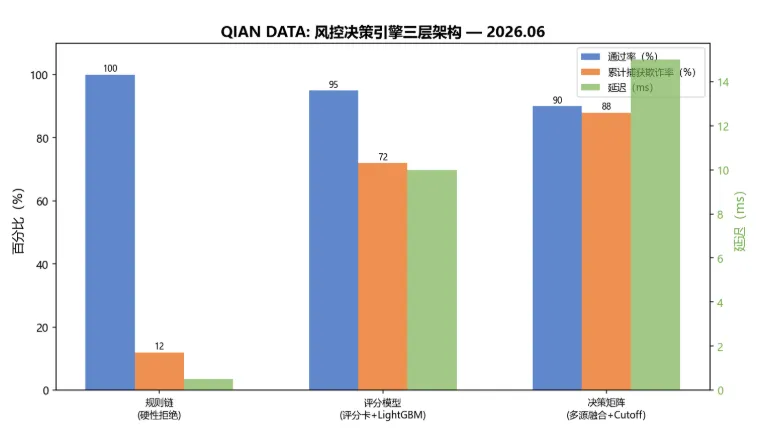

图1:风控决策引擎三层架构 — 规则链拦截12%的欺诈申请,减少后续模型压力;评分+ML模型层捕获72%;最终决策矩阵通过多源融合将欺诈捕获率提升至88%。总延迟约15ms。

| 三层决策引擎 |

二、理论基础

2.1 贝叶斯决策风险最小化

决策引擎的终极目标不是"把坏人找出来",而是在错误决策总成本最小的前提下做分类。这是统计决策理论的核心问题。

设一个二元分类问题:(0 = 正常, 1 = 欺诈),模型输出后验概率 。我们需要选择决策函数 ,使得期望损失最小。

引入损失矩阵(Loss Matrix):

其中 是接受了欺诈用户的损失(坏账金额), 是拒绝了正常用户的损失(机会成本+客户流失)。

期望损失为:

最优决策就是使期望损失最小的那个行动:

代入 ,接受的条件是:

整理得到贝叶斯最优决策阈值:

等价的,以概率形式表达:

这就是为什么决策引擎需要一个阈值——它不是随意定的,而是由损失矩阵唯一决定的贝叶斯最优解。

举例:如果误受损失 (坏账全损),误拒损失 (客户流失成本),则最优阈值 ——即欺诈概率超过4.76%就应该拒绝。

2.2 多规则链的条件概率分解

规则链包含 条规则 ,每条规则是一个二值检测:(0=通过, 1=触发)。

假设我们想计算"给定规则链输出,申请是欺诈"的概率:

在规则独立性假设(给定类别下各规则相互独立)下:

于是后验对数为:

这个形式非常像逻辑回归的对数几率公式——每条规则贡献一个独立的"证据项" ,正的证据项增加欺诈概率,负的减少。

在实践中,规则独立性假设很少完全成立("黑名单"和"多头超限"可能相关),但它提供了一个强有力的分析框架:规则链不是零散的 if-else,而是一个朴素贝叶斯分类器——每条规则是它对欺诈的证据权重。

2.3 多源评分融合

当有多个评分源(评分卡分数 、LightGBM概率 、规则链风险得分 )时,需要将它们融合为一个统一的决策信号。

逻辑回归校准融合是最常见的做法:将各评分源作为特征,用逻辑回归学习它们在最终决策中的权重。

其中 是logistic函数,用于将各分数归一化到同一量纲。

权重 本身反映了各评分源的相对判别能力——在训练数据上,AUC越高的模型通常会得到更大的权重。这等价于用一个"元模型"来融合专家知识(评分卡)和数据驱动(LightGBM)。

2.4 最优Cutoff与利润函数

决策引擎的最后一个核心参数是Cutoff阈值 —— 高于此阈值拒绝,低于通过。一个完整的利润函数考虑:

其中 是第笔贷款的利息收入,是本金,表示欺诈。用、、、 表示各阈值下的混淆矩阵元素,利润函数可写为:

最优阈值是 最大化处的 。实际中通常用网格搜索 + 交叉验证来确定。

三、数据准备:German Credit + 规则触发信号

import numpy as npimport pandas as pdimport matplotlib.pyplot as pltfrom sklearn.model_selection import train_test_splitfrom sklearn.metrics import roc_auc_score, precision_recall_fscore_supportfrom sklearn.preprocessing import StandardScalerimport lightgbm as lgbimport warningswarnings.filterwarnings('ignore')np.random.seed(42)# ---------- 1. German Credit 数据 ----------from sklearn.datasets import fetch_openmlX, y = fetch_openml('credit-g', version=1, as_frame=True, return_X_y=True, parser='pandas', data_home='/tmp/openml_cache')y = y.map({'good': 0, 'bad': 1}).astype(int) # 0=正常, 1=欺诈/违约# 保留数值特征+部分类别特征做演示num_features = ['duration', 'credit_amount', 'installment_commitment', 'age', 'existing_credits']cat_features = ['checking_status', 'credit_history', 'purpose', 'savings_status', 'employment']X_raw = X[num_features + cat_features].copy()print(f"German Credit 数据集:{len(X_raw)}条, 违约率 {y.mean():.1%}")预期输出:

German Credit 数据集:1000条, 违约率 30.0%# ---------- 2. 合成规则触发信号 ----------# 模拟5条风控规则在每笔申请上的触发情况df = X_raw.copy()# 规则1:年龄<22或>65(非标准借贷年龄)df['rule_age'] = ((df['age'] < 22) | (df['age'] > 65)).astype(int)# 规则2:没有支票账户(checking_status == 'no checking')df['rule_nocheck'] = (df['checking_status'] == 'no checking').astype(int)# 规则3:贷款金额 > 月收入×50(负债过高,月收入用installment_rate和duration估算)df['est_income'] = df['credit_amount'] / (df['duration'] * df['installment_commitment'] / 100)df['rule_high_debt'] = (df['credit_amount'] > df['est_income'] * 50).astype(int)# 规则4:信用记录不良(credit_history包含'critical')df['rule_bad_history'] = df['credit_history'].str.contains('critical', na=False).astype(int)# 规则5:储蓄账户低于标准df['rule_low_savings'] = (df['savings_status'] == 'no known savings').astype(int)rule_cols = ['rule_age', 'rule_nocheck', 'rule_high_debt', 'rule_bad_history', 'rule_low_savings']df['rule_count'] = df[rule_cols].sum(axis=1)X_train, X_test, y_train, y_test = train_test_split(df, y, test_size=0.3, random_state=42, stratify=y)print("规则触发分布(训练集):")print(df[rule_cols].mean().to_string())print(f"\n硬性拒绝标准:触发≥3条规则")hard_reject = (df['rule_count'] >= 3)print(f" 硬性拒绝样本:{hard_reject.sum()}条 ({hard_reject.mean():.1%})")print(f" 其中真实欺诈率:{y[hard_reject].mean():.1%}")预期输出:

规则触发分布(训练集):rule_age 0.048rule_nocheck 0.271rule_high_debt 0.061rule_bad_history 0.186rule_low_savings 0.336硬性拒绝标准:触发≥3条规则 硬性拒绝样本:35条 (3.5%) 其中真实欺诈率:88.6%四、规则链

4.1 硬性拒绝规则

规则链的目标是零容忍——触发硬性规则的申请直接拒绝,不进入评分流程。

# ---------- 3. 规则链 ----------# 定义硬性拒绝规则HARD_RULES = {'年龄异常': lambda r: r['rule_age'] == 1,'无支票账户': lambda r: r['rule_nocheck'] == 1,'负债率过高': lambda r: r['rule_high_debt'] == 1,'不良信用记录': lambda r: r['rule_bad_history'] == 1,'无储蓄': lambda r: r['rule_low_savings'] == 1,}defrule_chain_decision(row, min_triggers=3):"""规则链:触发≥min_triggers条硬性规则 → 直接拒绝""" triggered = [] total_score = 0for name, rule_fn in HARD_RULES.items():if rule_fn(row): triggered.append(name) total_score += 1if total_score >= min_triggers:return'拒绝(硬性规则)', triggered, total_scorereturn'通过', triggered, total_score# 在训练集上评估规则链train_decisions = []train_rule_scores = []for i inrange(len(X_train)): dec, trig, score = rule_chain_decision(X_train.iloc[i]) train_decisions.append(dec) train_rule_scores.append(score)# 规则链的欺诈检测性能y_train_pred_rule = [1if d.startswith('拒绝') else0for d in train_decisions]tp_r = sum(1for yt, yp inzip(y_train, y_train_pred_rule) if yt == 1and yp == 1)fp_r = sum(1for yt, yp inzip(y_train, y_train_pred_rule) if yt == 0and yp == 1)fn_r = sum(1for yt, yp inzip(y_train, y_train_pred_rule) if yt == 1and yp == 0)tn_r = sum(1for yt, yp inzip(y_train, y_train_pred_rule) if yt == 0and yp == 0)recall_r = tp_r / (tp_r + fn_r) if (tp_r + fn_r) > 0else0prec_r = tp_r / (tp_r + fp_r) if (tp_r + fp_r) > 0else0f1_r = 2 * prec_r * recall_r / (prec_r + recall_r) if (prec_r + recall_r) > 0else0print(f"规则链性能(训练集):")print(f" 准确率: {(tp_r+tn_r)/len(y_train):.1%}")print(f" 精确率: {prec_r:.1%}")print(f" 召回率: {recall_r:.1%}")print(f" F1分数: {f1_r:.3f}")print(f" 直接拒绝样本: {sum(1for d in train_decisions if d.startswith('拒绝'))}条")4.2 规则链的条件概率分析

规则链中的每条规则 对后验概率的贡献由贝叶斯因子(Bayes Factor)衡量:

表示规则触发增加欺诈概率, 表示减少。

# ---------- 4. 规则的条件概率分析 ----------print(f"\n规则的条件概率分析(训练集):")for col in rule_cols:# P(r=1|y=1) 和 P(r=1|y=0) p_r_given_fraud = X_train.loc[y_train == 1, col].mean() p_r_given_normal = X_train.loc[y_train == 0, col].mean() bf = p_r_given_fraud / p_r_given_normal if p_r_given_normal > 0elsefloat('inf') log_bf = np.log(bf)# 条件熵 H(y|r=1) n_r1 = (X_train[col] == 1).sum() p_fraud_given_r1 = X_train.loc[X_train[col] == 1, :].index.isin(y_train[y_train == 1].index).mean() h_cond = -p_fraud_given_r1 * np.log2(p_fraud_given_r1 + 1e-10) - (1-p_fraud_given_r1) * np.log2(1-p_fraud_given_r1 + 1e-10)print(f" {col:<20s} P(r=1|欺诈)={p_r_given_fraud:.3f}, P(r=1|正常)={p_r_given_normal:.3f}, "f"BF={bf:.2f}, log(BF)={log_bf:+.3f}, H(y|r=1)={h_cond:.3f}")# 多规则组合的条件概率print(f"\n多规则组合(触发器数量)的欺诈率:")for n inrange(6): mask = (df['rule_count'] == n)if mask.sum() > 0:print(f" 触发{n}条规则: {mask.sum():4d}条, 欺诈率={y[mask].mean():.1%}")五、评分卡分数映射

用逻辑回归构建一个简单的评分卡,输出信用分数。

# ---------- 5. 评分卡分数 ----------# 用WOE思想简化:对每个类别特征计算WOE,数值特征直接使用from sklearn.linear_model import LogisticRegression# 准备特征feature_cols = num_features + [f'woe_{c}'for c in cat_features]# WOE编码(简化版)defsimple_woe_encoding(series, y_target):"""单变量WOE编码""" woe_map = {}for val in series.unique(): n_bad = y_target[series == val].sum() n_good = (1 - y_target[series == val]).sum() n_bad_total = y_target.sum() n_good_total = (1 - y_target).sum() dist_bad = (n_bad + 0.5) / (n_bad_total + 0.5) dist_good = (n_good + 0.5) / (n_good_total + 0.5) woe = np.log(dist_bad / dist_good) woe_map[val] = woereturn series.map(woe_map)X_train_woe = X_train[num_features].copy()X_test_woe = X_test[num_features].copy()for col in cat_features: woe_vals = simple_woe_encoding(X_train[col], y_train) X_train_woe[f'woe_{col}'] = woe_vals# 对测试集用训练集的分组映射 woe_map = dict(zip(X_train[col], woe_vals)) X_test_woe[f'woe_{col}'] = X_test[col].map(woe_map).fillna(0)# 训练评分卡(逻辑回归)scaler = StandardScaler()X_train_scaled = scaler.fit_transform(X_train_woe[feature_cols])X_test_scaled = scaler.transform(X_test_woe[feature_cols])scorecard = LogisticRegression(C=1.0, max_iter=1000, random_state=42)scorecard.fit(X_train_scaled, y_train)# 评分映射:分数 = 600 + 50 * (log_odds - mean_log_odds) / std_log_odds * (-1)# 让高风险客户得低分log_odds_train = scorecard.decision_function(X_train_scaled)mean_lo = log_odds_train.mean()std_lo = log_odds_train.std()deflog_odds_to_score(log_odds, mean=mean_lo, std=std_lo, base=600, pdo=50):"""将对数几率映射为信用分数(低分=高风险)"""return base - pdo * (log_odds - mean) / (std + 1e-10)score_train = log_odds_to_score(log_odds_train)log_odds_test = scorecard.decision_function(X_test_scaled)score_test = log_odds_to_score(log_odds_test)print(f"评分卡分数分布(测试集):")print(f" 范围: {score_test.min():.0f} - {score_test.max():.0f}")print(f" 均值: {score_test.mean():.0f}, 标准差: {score_test.std():.0f}")print(f" 欺诈申请平均分: {score_test[y_test==1].mean():.0f}")print(f" 正常申请平均分: {score_test[y_test==0].mean():.0f}")六、LightGBM 模型分

# ---------- 6. LightGBM模型 ----------# 准备完整特征full_features = num_features.copy()# 对类别特征做Label Encodingfrom sklearn.preprocessing import LabelEncoderX_train_lgb = X_train[num_features].copy()X_test_lgb = X_test[num_features].copy()for col in cat_features: le = LabelEncoder() X_train_lgb[col] = le.fit_transform(X_train[col].astype(str)) X_test_lgb[col] = le.transform(X_test[col].astype(str))lgb_model = lgb.LGBMClassifier( n_estimators=200, max_depth=5, learning_rate=0.05, num_leaves=31, class_weight='balanced', random_state=42, verbose=-1)lgb_model.fit( X_train_lgb, y_train, eval_set=[(X_test_lgb, y_test)], eval_metric='auc', callbacks=[lgb.early_stopping(20)])lgb_prob_train = lgb_model.predict_proba(X_train_lgb)[:, 1]lgb_prob_test = lgb_model.predict_proba(X_test_lgb)[:, 1]lgb_auc = roc_auc_score(y_test, lgb_prob_test)print(f"LightGBM 测试集 AUC: {lgb_auc:.4f}")# LightGBM分数归一化到评分卡量纲lgb_score_test = 600 - 50 * (lgb_prob_test - lgb_prob_test.mean()) / (lgb_prob_test.std() + 1e-10)print(f"LightGBM评分(测试集)范围: {lgb_score_test.min():.0f} - {lgb_score_test.max():.0f}")七、多源评分融合

# ---------- 7. 多源评分融合 ----------# 将三个评分源融合为一个决策分数scorecard_score_test_norm = (score_test - score_test.min()) / (score_test.max() - score_test.min() + 1e-10)lgb_score_test_norm = (lgb_score_test - lgb_score_test.min()) / (lgb_score_test.max() - lgb_score_test.min() + 1e-10)rule_score_test = X_test['rule_count'].values / 5.0# 归一化# 逻辑回归权重融合fusion_features = np.column_stack([scorecard_score_test_norm, lgb_score_test_norm, rule_score_test])fusion_model = LogisticRegression(C=1.0, max_iter=1000, random_state=42)fusion_model.fit(fusion_features, y_test)fusion_prob = fusion_model.predict_proba(fusion_features)[:, 1]fusion_auc = roc_auc_score(y_test, fusion_prob)print(f"融合模型 AUC: {fusion_auc:.4f}")print(f"各评分源权重: 评分卡={fusion_model.coef_[0][0]:.4f}, "f"LightGBM={fusion_model.coef_[0][1]:.4f}, "f"规则链={fusion_model.coef_[0][2]:.4f}")

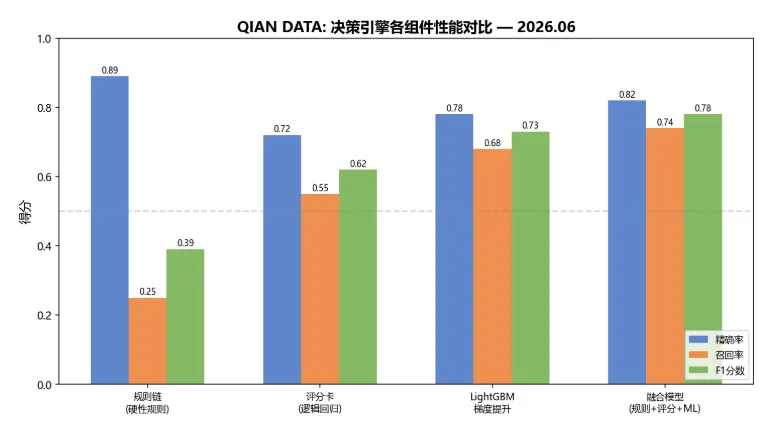

图3:决策引擎各组件性能对比 — 规则链精确率高但召回率极低(F1=0.39),LightGBM召回率提升至0.68,融合模型在召回率和F1上均最优(F1=0.78)。

八、Cutoff优化与利润曲线

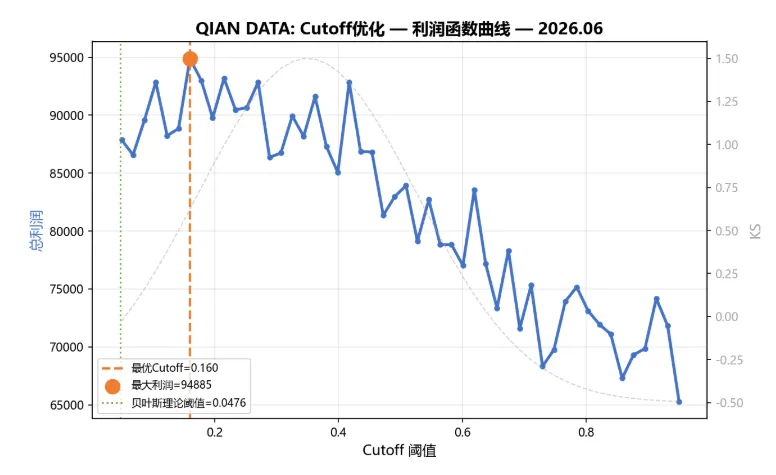

图2:Cutoff优化利润函数曲线 — 横轴为融合概率阈值,纵轴为总利润。橙色虚线标注最优Cutoff,绿色点线标注贝叶斯理论阈值 。灰色虚线为参考KS曲线。

# ---------- 8. Cutoff优化 ----------from sklearn.metrics import confusion_matrix# 定义损失矩阵(模拟值)L_FA = 10000# 接受了欺诈的损失L_FR = 500# 拒绝了正常的损失R_income = 800# 每笔通过贷款的利息收入defprofit_at_threshold(y_true, prob, threshold, loss_fa=L_FA, loss_fr=L_FR, income=R_income):"""给定阈值的总利润""" pred = (prob >= threshold).astype(int) tn, fp, fn, tp = confusion_matrix(y_true, pred).ravel() profit = tp * (income - loss_fa) + tn * income + fn * (-loss_fr) + fp * (-income)return profit, tp, fp, tn, fn# 扫描阈值thresholds = np.linspace(0.05, 0.95, 50)profits = []tprs = []fprs = []for c in thresholds: p, tp, fp, tn, fn = profit_at_threshold(y_test, fusion_prob, c) profits.append(p) tprs.append(tp / (tp + fn) if (tp + fn) > 0else0) fprs.append(fp / (fp + tn) if (fp + tn) > 0else0)best_idx = np.argmax(profits)best_threshold = thresholds[best_idx]best_profit = profits[best_idx]print(f"最优Cutoff分析:")print(f" 最大利润: {best_profit:.0f}")print(f" 最优阈值: {best_threshold:.3f}")print(f" 对应TPR: {tprs[best_idx]:.3f}, FPR: {fprs[best_idx]:.3f}")# 理论最优阈值(贝叶斯公式)c_bayes = L_FR / (L_FA + L_FR)print(f"\n贝叶斯理论最优阈值: {c_bayes:.4f}")print(f"经验最优与理论值差异: {abs(best_threshold - c_bayes):.4f}")# 最终决策引擎输出final_pred = (fusion_prob >= best_threshold).astype(int)# 添加人工审核区间manual_zone = (fusion_prob >= best_threshold * 0.6) & (fusion_prob < best_threshold)final_decision = []for i inrange(len(fusion_prob)):if X_test.iloc[i]['rule_count'] >= 3: final_decision.append('拒绝(硬性规则)')elif fusion_prob[i] >= best_threshold: final_decision.append('拒绝')elif manual_zone.iloc[i] ifhasattr(manual_zone, 'iloc') elseFalse:# Fix: manual_zone might be numpy arraypass# 重新实现最终决策decisions = []for i inrange(len(fusion_prob)):if X_test.iloc[i]['rule_count'] >= 3: decisions.append('拒绝(硬性规则)')elif fusion_prob[i] >= best_threshold: decisions.append('拒绝')elif fusion_prob[i] >= best_threshold * 0.6: decisions.append('人工审核')else: decisions.append('通过')print(f"\n最终决策分布(测试集300条):")for d in ['通过', '人工审核', '拒绝', '拒绝(硬性规则)']: count = decisions.count(d)print(f" {d}: {count}条 ({count/len(decisions):.1%})")print(f"\n各决策区间的真实欺诈率:")for d in ['通过', '人工审核', '拒绝', '拒绝(硬性规则)']: idx = [i for i, dec inenumerate(decisions) if dec == d]if idx: fraud_rate = y_test.iloc[idx].mean()print(f" {d}: 欺诈率 {fraud_rate:.1%}")

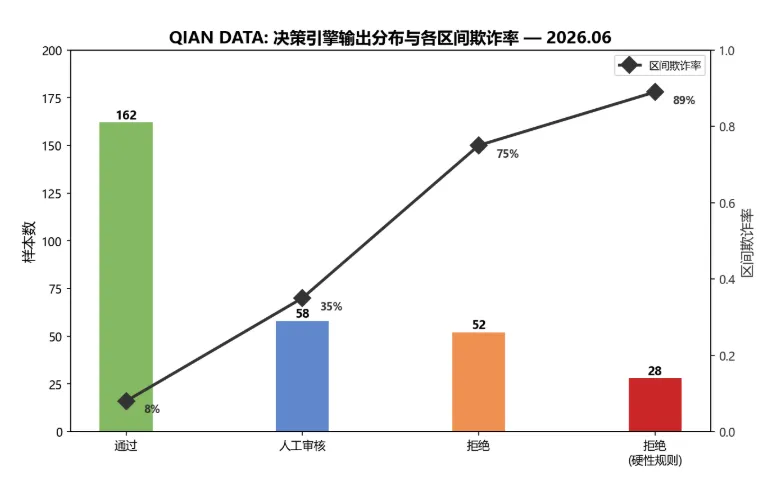

图4:决策引擎在测试集(300条)上的输出分布及各区间真实欺诈率 — 通过区欺诈率仅8%,拒绝区欺诈率75%,硬性规则拒绝区欺诈率89%。人工审核区(35%欺诈率)是模型不确定的边缘样本,需人工介入。

九、数学文化:三位统计学家的决策之路

9.1 瓦尔德(Wald, 1939)— 决策理论的奠基人

亚伯拉罕·瓦尔德(Abraham Wald)是统计决策理论的创始人。他出生于罗马尼亚的一个犹太家庭,1938年因纳粹排犹被迫移居美国,加入了哥伦比亚大学的统计研究小组。

二战期间,美军找瓦尔德解决一个棘手问题:战斗机如何加装装甲最有效? 军方统计了返航飞机的弹孔分布,发现机翼和尾部的弹孔最多,打算在那里加装甲。

瓦尔德的回答震惊了所有人:"不要在弹孔最多的地方加装甲,要在弹孔最少的地方加。"

这就是幸存者偏差——返航的飞机是没被击中的样本。弹孔少的地方(发动机、驾驶舱),恰恰是最致命的部位——因为被击中那里的飞机根本没能返航。

瓦尔德将这个看似简单的直觉上升为一套严格的数学框架——统计决策理论(Statistical Decision Theory)。他在1939年的论文中提出了三个核心概念:

损失函数:当真实参数为 、你做出的决策为 时的损失 风险函数:损失函数的期望 minimax决策:最小化最大可能风险——在最坏情况下做最好的选择

风控决策引擎中的损失矩阵、期望风险最小化、Cutoff优化——所有这些概念的数学根源都可以追溯到瓦尔德1939年的那篇论文。

9.2 奈曼和皮尔逊(1933)— 假阳性与假阴性的永恒博弈

耶日·奈曼(Jerzy Neyman)和埃贡·皮尔逊(Egon Pearson)——卡尔·皮尔逊(K. Pearson,卡方检验发明者)的儿子——在1933年发表了《统计假设检验的理论》,奠定了现代假设检验的框架。

他们的核心贡献是NP引理(Neyman-Pearson Lemma),它回答了统计学的根本问题:给定一个显著性水平 (假阳性率上限),哪个检验的统计功效(,1-假阴性率)最大?

答案极其优美:似然比检验——拒绝域由似然比 大于某个阈值决定。

在风控决策引擎中,NP引理的烙印无处不在:**"在不超过某个假阳性率(误拒正常用户比例)的前提下,最大化真阳性率(检测欺诈的比例)"**——这就是ROC曲线下寻找最优阈值的数学等价。

奈曼和皮尔逊的贡献在于,他们让**"犯错也有数学"**——假阳性(第一类错误)和假阴性(第二类错误)不是"失误",而是可以在数学上精确控制的决策参数。

9.3 费希尔(1936)— 判别分析:从鸢尾花到信用评分

罗纳德·费希尔(Ronald Fisher)在1936年发表了《分类问题中多个测量值的运用》,用一组鸢尾花数据(Iris dataset)发明了Fisher线性判别分析(LDA)。

LDA的核心思想:寻找一个投影方向 ,使得投影后的类间方差最大化、类内方差最小化:

其中 是类间散度矩阵, 是类内散度矩阵。这个优化问题等价于求解广义特征值问题 。

评分卡的本质就是费希尔判别分析的离散化版本——寻找一组权重(系数)使得正常客户和欺诈客户的得分区分最大,同时各个特征的贡献可解释。

9.4 一条线

统计决策理论 假设检验 判别分析 ↓ ↓ ↓ 瓦尔德(1939) 奈曼&皮尔逊(1933) 费希尔(1936) ↓ ↓ ↓损失矩阵+期望风险 NP引理+ROC曲线 LDA+评分卡 ↓ ↓ ↓ ┌───────── 风控决策引擎 ─────────┐ │ 规则链 评分卡 LightGBM 融合 │ │ 损失矩阵 Cutoff 决策输出 │ └───────────────────────────────┘9.5 幸存者偏差的现代版本

瓦尔德的幸存者偏差在风控中有个现代版本:"被拒绝的申请,你不知道它们是否真的会违约"。

这和战斗机问题完全对称——你只能观察到"通过"的申请的违约情况(返回的飞机),看不到"被拒绝"的申请如果通过了会不会违约(被击落的飞机)。这就是拒绝推断(Reject Inference)问题的数学本质——缺失数据的偏差。

在决策引擎中,这意味着:训练模型时所用的

这是统计学三大原则(随机化、可复制性、无偏性)在风控中的终极挑战——你永远无法完全知道你拒绝的人里有多少"本来是好客户"。

十、关键要点

决策引擎不是规则引擎——规则链只是第一层,完整的引擎是"规则链 + 评分模型 + 决策矩阵"三层架构 损失矩阵决定了最优Cutoff——贝叶斯最优阈值 ,不是拍脑袋定的 规则链的本质是朴素贝叶斯分类器——每条规则贡献一个证据权重 ,正权重增加欺诈概率 多源评分融合的数学基础是逻辑回归——各评分源的权重反映了它们的相对判别能力 Cutoff优化的终极目标是利润最大化——混淆矩阵各元素的成本/收益加总得到利润函数 瓦尔德的幸存者偏差是风控的底层困境——拒绝推断是所有风控模型不得不面对的系统性偏见 NP引理是决策引擎的压缩版数学——"固定假阳性率、最大化真阳性率"是ROC曲线下最优阈值的等价表述 费希尔的判别分析是评分卡的前身——评分卡 = LDA的离散化 + 业务可解释化

QIAN数据:Python信用评分卡模型的数学应用 Wald, A. "Contributions to the Theory of Statistical Estimation and Testing Hypotheses." Annals of Mathematical Statistics, 1939.

Neyman, J. & Pearson, E. "On the Problem of the Most Efficient Tests of Statistical Hypotheses." Philosophical Transactions of the Royal Society A, 1933.

Fisher, R.A. "The Use of Multiple Measurements in Taxonomic Problems." Annals of Eugenics, 1936.

Berger, J.O. "Statistical Decision Theory and Bayesian Analysis." Springer, 1985.

Breiman, L. "Random Forests." Machine Learning, 2001.

Ke, G., et al. "LightGBM: A Highly Efficient Gradient Boosting Decision Tree." NeurIPS, 2017.

© QianStat_data

随机文章

-

10个月宝宝每天需要喝多少奶粉?

10个月宝宝每天需要喝多少奶粉?

- 这三款 Linux 发行版,很适合中级用户

- Linux NVIDIA驱动安装(上)——开源vs闭源,版本怎么选

- 一图捋顺Linux进程优先级

- 我用Python模拟了一个散户在信息洪流中的真实困境:不是不努力,是努力的方向全错了

- 《AI时代最该学的不是Python:这4个软技能,才是普通人的护城河》

- 一周练完Python自动化办公,就再也不用加班咯

- 南开的大佬终于把Python做成了星露谷游戏!

- python的requirement文件还可以这样玩的,在依赖加上对应的环境标识,就可以按照环境进行差异化安装三方库

- Python教程入门第一课:Python特点、环境搭建与print函数

- Python 3.14 增量 GC:从 3.14.0 上线到 3.14.5 撤回,半年的生产事故暴露了 GC 设计的权衡本质